On the History and Future of Money

When money is easy to make, society starts to break

There is something off in the world. Most of us can feel it, even if we cannot name it.

The older generation worked hard, saved carefully, and paid into pension systems, and is now watching those very savings buy less every year.

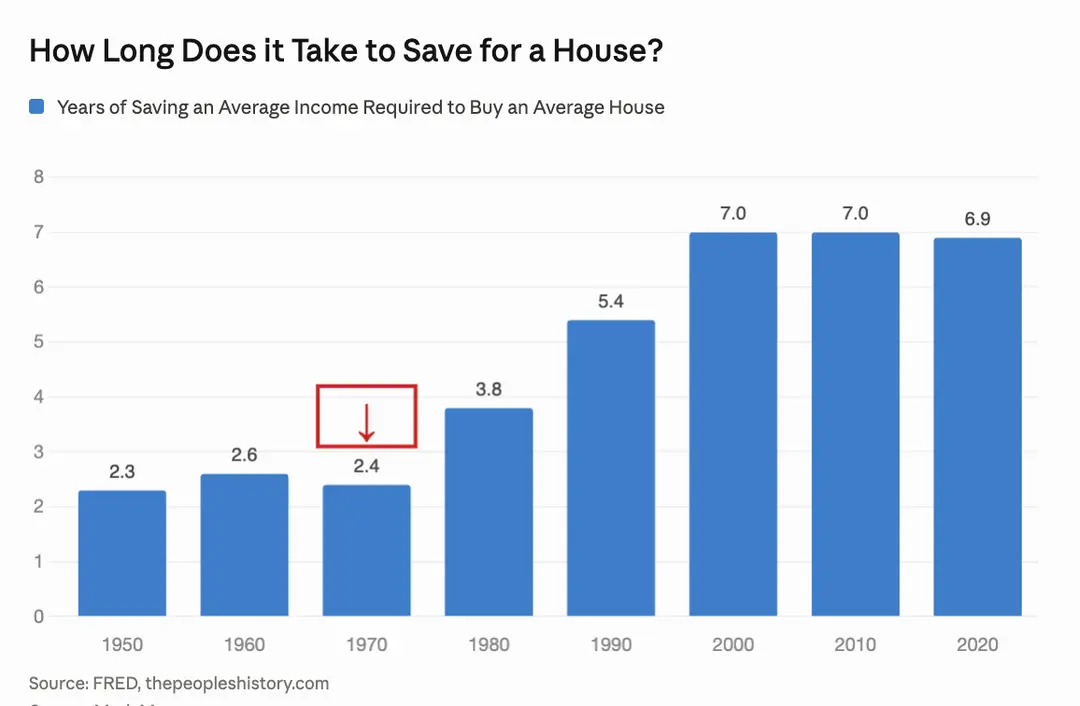

Their children did everything they were told and still struggle to afford the life their parents had. Saving for a house takes three times longer, they finish school later, take longer to move out and start a family.

Money doesn't work anymore.

But to unpack that, we need to start with a question almost nobody asks.

What Is Money?

Money is a medium to store and transfer favors. You help someone and receive a token which you can exchange for help in the future. This is called deferred reciprocity.

The best analogy for money is a battery. You charge it and you deplete it. You charge it by producing for others and drain it by consuming the time, energy and effort of others.

It's an external score-card of who owes who.

The History Of Money

When humans lived in hunter-gatherer tribes we kept these scores internally. You help me hunt today, I will help construct your house tomorrow. It's a simple tit-for-tat exchange of value. The same way we trade favors with friends.

No need to write it down since the number of trades, people and surplus resources were limited. We could simply keep it in our heads.

Flash-forward to around 10,000 years ago, where we settled in one place and started farming. Agriculture made population skyrocket. All of a sudden we had fields to protect, surpluses to store and excess to trade.

We invented the written language to externalize these mental score-cards. Like the Sumerian clay tablets to track payments in grain. Our earliest writings were ledgers and financial records, not stories or diaries.

Throughout history this externalized score-card has been almost anything; clay tablets, salt, beads, stone, wheat, tobacco, shells, steel, iron, gold, silver, animals, bronze bracelets, humans, and more.

However, not all items make good ledgers. Apples spoil, metals rust, shells are all different, salt is abundant, stones are heavy, and so on. The best money checks all these boxes:

- Medium of exchange: it can easily change hands

- Unit of account: calculations can be made with it

- Store of value: it holds its purchasing power over time

- Divisible: it should be usable for small and big transactions

- Durable: it should last over time

- Portable: it should be easy to transport

- Fungible: Each unit is interchangeable

- Private: To prevent theft, it should be easy to hide

- Saleable: it should be widely accepted

Over time (and after many failed attempts), completely independent from each other, different cultures eventually settled on precious metals (gold and silver mainly). Because gold and silver scored the best on all these criteria.

Over time, the ruling authority standardized these metals by casting them into coins similar in size and weight.

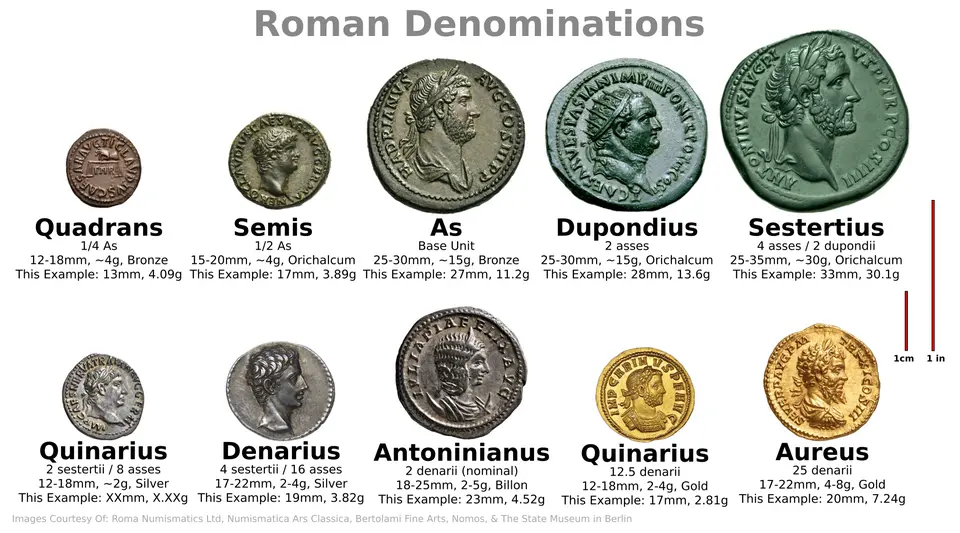

The shekel, aureus, denarius, sestertius, florins, pieces of eight, the pound (of silver), ... .

With a standardized medium of exchange, we could do away with scales and society flourished. A stable SI-unit of value gave rise to the great Roman Empire.

However the problem with issuing your own money is the temptation to dilute it and spend beyond what you have received.

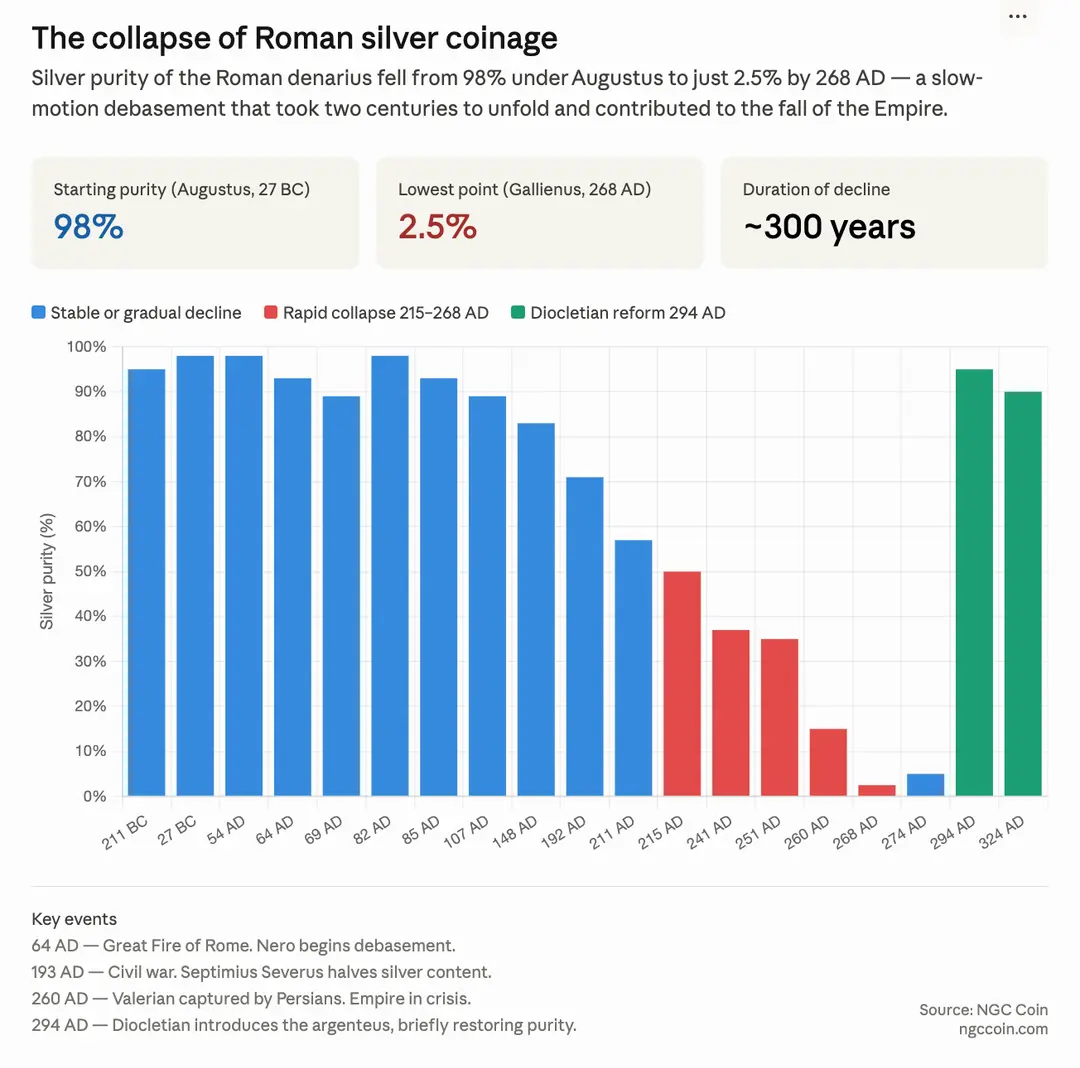

The Roman government started to issue new coins with the same face value but lower precious metal content.

By reducing the purity and size of the coins they collected as taxes (by re-melting and diluting), governments could create more coins and spend more than they earned through taxation. Making them noticeably darker and smaller.

Effectively transferring purchasing power from the saver to the issuer without their consent nor knowledge. And over time pushing up all prices.

Silver denarius before and after debasement.

Money Today

Until 1971, gold has been money in one form or another. We moved it into bank vaults because it was slow to move and prone to theft. But still, gold was the base layer.

Paper banknotes were tied to a fixed amount of gold, and could be traded in at a bank. Hence the phrase "we promise to pay the bearer on demand" on banknotes. A Great Britain "pound" could be changed for an actual pound of silver.

Paper money was basically a claim ticket on gold.

But still the same incentive to create more banknotes than you kept gold in the vault appeared. The technology changes, the incentives don't.

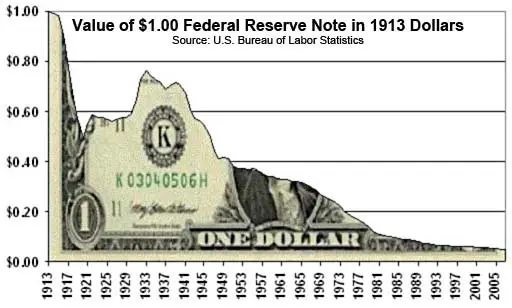

This allowed the US to buy things at only the cost of printing their own money for a long time. When France realized this, and president Charles De Gaulle started converting their numerous dollars back into gold, president Nixon ended the gold standard. Effectively defaulting on their promise.

And since that point in time, no currency is tied to a natural limit anymore. They are free-floating and limited only by the trust of their holders.

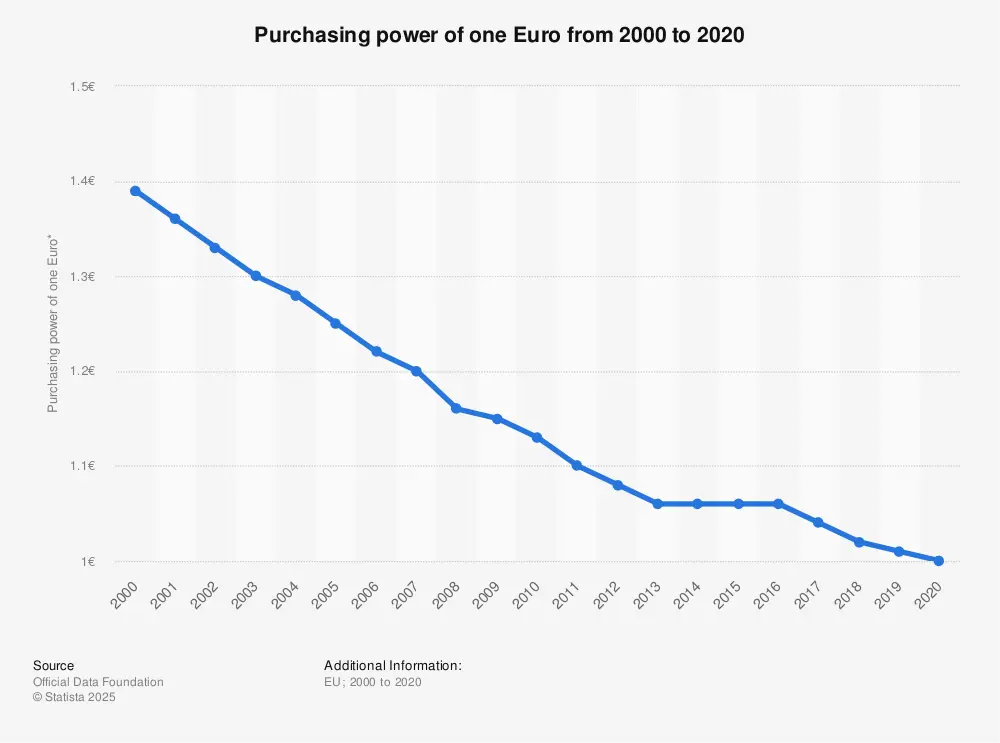

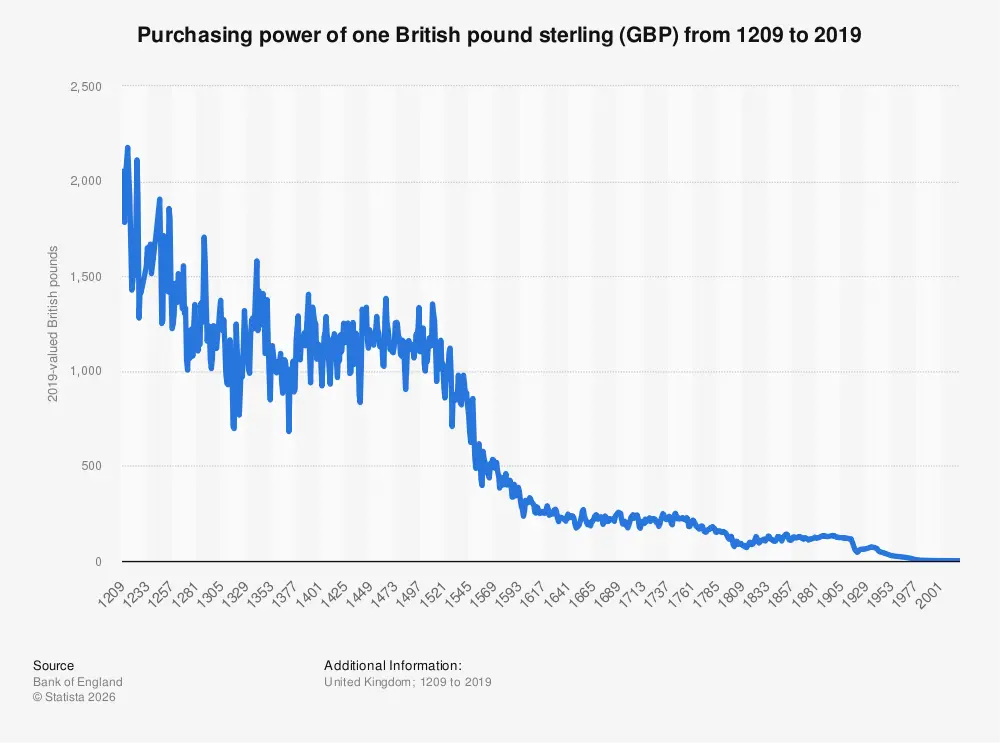

Without this natural limit, most major currencies have already lost a significant amount of their purchasing power over time.

History repeats: Ancient Greece, Germany, Lebanon, Venezuela, Zimbabwe, Turkey, Argentina, Hungary, Egypt, Sri Linka. But also bigger markets like the US, UK and eurozone have the same incentive problem.

Different rates, different reasons, but they all go in the same direction.

Find more statistics at Statista

We have gotten so used to inflation we see it as natural. Our contracts reflect it, we expect wages to increase, and our entire society strategizes how to benefit from it.

We have built whole industries: wealth management, financial planning, inflation-linked bonds that thrive solely because every year money slowly dies.

The natural state of a growing economy is deflation: Prices going down over time. More productivity means more goods, means lower prices and a higher standard of living for everyone.

But that only works if the value can flow to the saver. But through inflation, it gets captured at the top, by whoever is closest to the printer.

A monopoly on money leads to predictable problems.

- Saving is ineffective and we financialize real estate. Hurting the younger generations' ability to buy a home and start a family.

- Wealth gaps increase between the have-assets and have-savings. Wealth creation becomes less meritocratic and just reflects proximity to whoever controls the mint.

- Less people in society (can) focus on just producing goods and services. We all need to become wealth planners or become heavily reliant on them.

- Real tax rates increase because inflation pushes wages, stocks and assets in higher brackets without actually increasing purchasing power or requiring new legislation (consent).

- Reduced limit on government expenditure. Leading to misallocation of public funds, wars that last too long, bailouts for banks that deserved to fail, bloated bureaucracies, vanity projects and bottomless subsidies to cronies.

- Erosion of the pension system. Effectively defaulting on a promise to a group of society that can't fight back anymore.

- Centralization quietly increases the ability for financial repression and capital controls: Confiscation, debanking, bail-ins, surveillance, social credit systems, tax rates beyond consent of the governed.

The people who do well in this system are the ones that can borrow large amounts at low rates over long periods to buy real things: property, land, stocks and commodities. Especially when positioned close to the mint or able to write their own rules.

The Future Of Money

The world would benefit greatly from a free-market competition in money. This idea isn't new, it just hasn't been allowed to exist.

We had attempts at Free Banking in the US, Ireland, Scotland, the Liberty Dollar, E-gold and more recently with the Facebook Libra. All suppressed, once they became too successful. Not because they failed, but because they worked.

Free banking worked because banks issued their own paper notes redeemable for gold on demand. Bank A that issued too much would be held accountable by Bank B through bank runs. Competition is what keeps markets honest - Monopolies do the opposite.

Hayek talked about this extensively in his essay on "the denationalization of money"

Inflation, instability, undisciplined state expenditure, economic nationalism - have a common origin and a common cure: the replacement of the government monopoly of money by competition in currency supplied by private issuers who, to preserve public confidence, will limit the quantity of their paper issue and thus maintain its value.

Money is no different from other commodities and would be better supplied by competition between private issuers than by a monopoly of government

Milton Friedman argued the same;

The Great Depression in the United States, far from being a sign of the inherent instability of the private enterprise system, is a testament to how much harm can be done by mistakes on the part of a few men when they wield vast power over the monetary system of a country. Any system which gives so much power and so much discretion to a few men that mistakes can have such far-reaching effects is a bad system. Money is much too serious a matter to be left to the Central Bankers

The future of money will be digital. That is certain.

Cash - for all its great qualities - is receding from society. Shops go cashless, banks close branches and ATM's disappear. Each step framed as convenience or crime prevention.

Cash is the last payment method that leaves no trace: anonymous, ungovernable, impossible to freeze. A relic of a freer time. If cash were invented today, it would meet the same fate as free banking.

Something will fill that gap. Two alternatives will compete for the future of money: cryptocurrency (free market money) and the CBDC (sovereign money), with existing banks wedged in the middle.

Which version will capture the trust of its holders is the real question.

Since 2009 we've seen the rapid adoption of crypto-currencies. We've seen free-floating ones like Bitcoin and ones that tokenize existing assets like Tether (Dollar), EURC (Euro) or PAXG (Gold).

This adoption has been most prominent in countries where capital controls are strictest and local currencies most unstable.

The reason cryptocurrencies succeeded where free-banking has failed, is two-fold:

- For Bitcoin, because it was engineered to be impossible to kill. To shut it down you would need to turn off every computer running the Bitcoin software, in every country, at the same time, forever. Unenforceable.

- For stablecoins because they didn't threaten or try to replace the existing central bank money. But simply extended the rails from private bank databases to public blockchains (read: shared databases) which broadened the market size.

And for both; because no-one truly understood it, until it had already grown too large.

Once major players (BlackRock, major banks, pension funds, ...) hold crypto assets on their balance sheets, shutting it down means wiping out their holdings. These are the same institutions that fund political campaigns and have direct lines to treasury departments.

This would be political suicide and look authoritarian to the public instead of prudent. Image is still a concern.

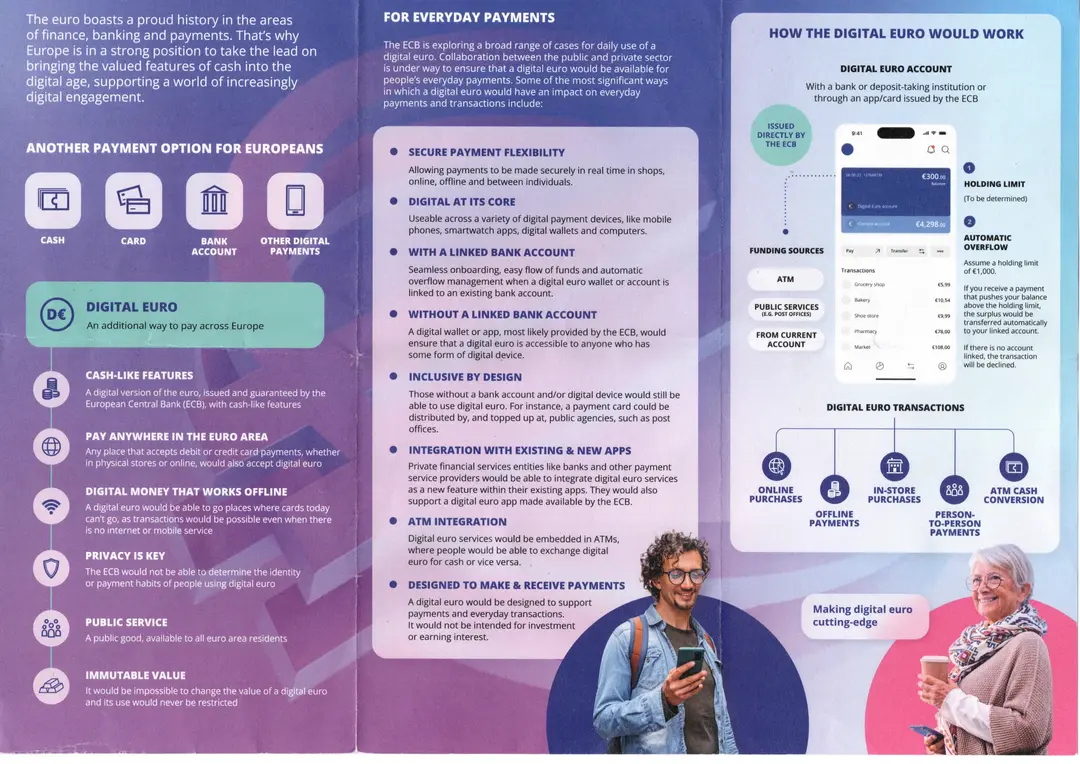

As response to this threat to sovereingty, we're seeing a push towards a digital euro, digital dollar, digital pound and digital yen. The central bank digital currency (CBDC) as state alternative before private players capture the market further - A direct bank account with the government.

The pitch is financial inclusion and cheaper transfers but the covert prize; better tax enforcement. The first two are real problems, but stablecoins already solved them better. And the third is really not a technical problem, but a consent issue.

The modern world simply does not consent to its tax rate anymore. You cannot fix a consent issue with a compliance hammer.

The implementation of the digital renminbi (e-CNY) in China is instructive and cautionary:

- Programmable restrictions - Money that expires or can't be spend on certain categories.

- Spending limits/saving caps. Limiting the amount you can receive, send or hold.

- Direct unbanking - Revoking your right to earn and spend at the push of a button.

- Total financial surveillance. Every transaction monitored, grouped, profiled and analyzed.

It is omitted from the brochure, but that's what the technology enables. And I doubt it'll be fully open source to allow anyone to verify.

The outcome depends entirely on what people choose to save in. The strength and stabillity of a currency solely depends on the number of people willing to hold it. Coercion can sway that balance, but not change that fact.

I'm still optimistic, given that in any jurisdiction where CBDC's are launched, the adoption remains low. For the simple fact that it doesn't solve a real problem. (See Human Rights Foundation - CBDC Tracker).

A society that accepts and saves in programmable, limited, revocable money has handed over something it will never get back: the right to earn, save and spend without needing permission. We already have public, open-source alternatives. Let the market decide which one wins.

In the short term, I believe the world will trend toward more surveillance and authoritarianism dressed up as crime prevention or child protection. But just as the printing press destroyed the church's monopoly on information, cryptocurrency holds that promise for the monopoly on money.

And society will be better off because of it.

Further reading

- The denationalization of money - Friedrich Hayek

- Capitalism and freedom - Milton Friedman

- Sapiens - Yuval Noah Harari

- Broken Money - Lyn Alden

- The Ascent of Money - Nial Ferguson

- How an economy grows and why it crashes - Peter D. Schiff

- The Bitcoin Standard - Saifedean Ammous

- wtfhappenedin1971.com

- History of Money Documentary

- Tradingeconomics.com

- https://www.longtermtrends.net/

- Wikimedia Commons for illustrations

Comments/Questions